- Reason #1: Renters insurance is affordable

- Reason #2: Renters insurance covers your stuff when you’re at home, and out and about

- Reason #3: Your personal property is probably worth more than you think

- Reason #4: Your landlord’s insurance won’t cover losses to your personal property

- Reason #5: Renters insurance covers dog bites

- Reason #6: Renters insurance may help you out if you're forced out of your apartment

- Reason #7: Renters insurance covers medical costs for injured guests

- Reason #8: Renters insurance may cover the costs to get you out of a jam if you're sued

- Other reasons to get renters insurance

- When is renters insurance required?

- How much renters insurance do you need?

With inflation reaching levels not seen in five decades—sending prices soaring for everything from food to housing—millions of renters find themselves considering which expenses are truly essential and which ones they can forgo.

Take renters insurance. Many landlords and property managers require their tenants to carry it. But even if you aren’t required to purchase insurance, getting covered is a no-brainer.

More and more renters are embracing renters insurance as a low-cost way to protect their property and peace of mind, with 57% of renters holding insurance in 2020, up from just 31% in 2012, according to the Insurance Information Institute.

Whether you’re already part of the insured majority and wondering whether keeping your coverage is worth it, or you’re weighing whether to purchase a renters insurance policy for the first time, let’s take a closer look at why getting insured is a smart financial decision.

Reason #1: Renters insurance is affordable

The average cost of renters insurance is around $23 per month as of 2025, with Lemonade’s renters insurance policies starting as low as $5 a month.

What do you get in exchange? We’ll dive into more detail on what renters insurance covers below, but perhaps the biggest benefit to buying renters insurance is knowing that your insurer will have your back in many of those inevitable “oh s!@#” moments. Like when you check your bag and realize your phone was stolen on the subway, or you come home to find that someone took your bike.

Reason #2: Renters insurance covers your stuff when you’re at home, and out and about

Who knew, right? So if your phone is stolen from your local coffee shop, or your laptop is picked up from your co-working space – your policy has your back. Yep, that’s right – even if your stuff is stolen outside of your home, renters insurance will reimburse you.

Plus, if your kitchen goes up in flames or your sprinklers go off accidentally and flood your apartment, you’re also covered. Talk about peace of mind!

Reason #3: Your personal property is probably worth more than you think

Many people may not realize the value of carrying renters insurance because they don’t realize just how valuable their personal property is.

Consider the average two-bedroom apartment in the US, which according to US News includes about $30,000 worth of electronics, clothing, jewelry, bikes, and more.

Armed with renters insurance, you’ll sleep easier at night knowing that should your personal belongings be lost, damaged, or destroyed by a covered event—like a fire, lightning, windstorm, theft, or vandalism—your personal property coverage can help cover the costs of replacing those items. Without renters insurance, you’d be on the hook for those expenses.

A pretty good reason to get covered, right? Once you’ve decided to buy renters insurance, you’ll want to take a quick look around your place to estimate the value of your stuff, so you can select the right coverage amount for your personal property.

Lemonade makes it easy to view and customize your coverage amounts through our app and website, so you’re covered for what you need.

Reason #4: Your landlord’s insurance won’t cover losses to your personal property

Since your landlord carries landlord insurance, you might be wondering: What’s the point of purchasing my own renters insurance policy?

It turns out that landlord insurance and renters insurance don’t cover the same things—most notably, while your landlord’s policy will cover any property they own, it won’t cover your personal belongings. All the more reason to get yourself protected.

Reason #5: Renters insurance covers dog bites

If you have a furry BFF and were wondering, “Does renters insurance cover dog bites?“ you’re in luck. If your dog bites someone, your policy has you covered. Better yet, your coverage applies whether your pup nips someone at your home or at the park.

There are two exceptions, though: You’re not covered if your dog has a history of biting, or if your dog is categorized as high-risk.

Reason #6: Renters insurance may help you out if you’re forced out of your apartment

If a kitchen fire forces you out of your apartment, or your upstairs neighbor leaves their faucet running all day and floods your apartment – your policy may cover something called loss of use. It helps you out with temporary housing and some other basic living expenses until your pad is habitable again.

Reason #7: Renters insurance covers medical costs for injured guests

Let’s be real: Stuff happens all the time when you aren’t paying attention and your friends sometimes get hurt at your place. Whether your dog decides to take a chunk outta your bestie (see #6), or your neighbor cuts themselves while helping you prep dinner—been there, done that—their injuries are most likely covered.

If it’s something small (read: under $5,000), your coverage for medical payments to others will kick in, but if your friend decides to take some unfriendly steps and sues you, your renters liability coverage will have your back. We’ll discuss liability more in the next section.

Reason #8: Renters insurance may cover the costs to get you out of a jam if you’re sued

This is what we call liability coverage in insurance speak. It protects you in cases where someone claims to be injured due to your actions or negligence. Your renters insurance will cover legal fees if you need a lawyer to defend you, and will also pay to cover damages you’re found liable for.

So, that neighbor who cut his finger in your kitchen? Say he went to the hospital, got stitches, and then sued you for the cost—your liability coverage may jump in to save the day.

Liability coverage normally starts at around $100,000, which isn’t a small chunk of change. But it can make a huge difference when legal bills and medical fees start racking up. If you find yourself asking “How much renters insurance do I need?“ looking at your lifestyle is a good place to start. Are you a risk-taker? Do you have a dangerous profession? Be honest with yourself and choose what makes sense for you.

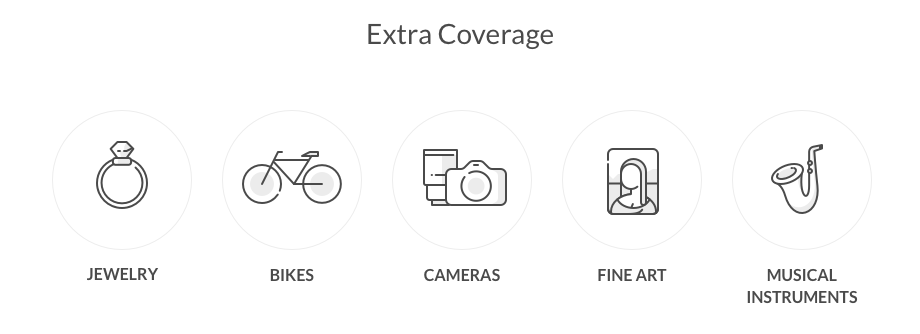

Other reasons to get renters insurance

There are some renters insurance benefits that come as add-ons to your basic renters insurance policy. They have to do with the things and people you value most!

Physical items such as expensive cameras, jewelry, and fine art can all be covered – they just aren’t part of your typical renters insurance policy. That’s because when you sign up for an insurance policy, you choose a coverage limit. But oftentimes, burglars will want to steal your most cherished and expensive things! We can’t let them get away with that.

This type of coverage protects your valuables from almost anything, including loss! So let’s say someone breaks into your apartment and steals your favorite (and most expensive) watch. Once you add scheduled personal property coverage, renters insurance will have your back!

Will this extra coverage break the bank, you ask? Luckily, this add-on will only cost you a few extra bucks a month, depending on your insurer. And protecting the stuff you love most is definitely worth that extra peace of mind (and the cost of a large latte!).

A standard renters insurance policy protects your electronics and appliances against certain “perils,” but not against every type of damage. For instance, if your washing machine has an electrical failure your base policy wouldn’t help. But if you want to add on those extra protections, you can purchase Equipment Breakdown Coverage (EBC). Also known as Appliance Coverage, this is an endorsement to complement and enhance your renters insurance and provide coverage for many other types of damage.

You can also add other people to your policy. While a typical policy automatically covers any resident of your household related by blood, marriage, or adoption, your sig others are not. They need to be added to your policy as what’s called an ‘additional insured.’ There is a charge for that, so keep in mind that sometimes it is cheaper or easier for each of you to get your own insurance policy.

FYI – roommates aren’t covered by a typical renters insurance policy. You’ll have to tell them to get their own!

When is renters insurance required?

As we mentioned, landlords or property managers occasionally may require proof of renters insurance under the terms of your lease.

Even if your lease doesn’t mandate renters insurance, though, purchasing a policy can keep your costs down in the event of a covered loss, whether it’s a burst pipe, a kitchen fire, or the theft of your smartphone. The right way to think about renters insurance isn’t in terms of whether you’re forced to have it, but rather by considering what could go wrong if you don’t have it.

How much renters insurance do you need?

There’s no one-size-fits-all answer, but to figure out how much renters insurance coverage you need, you’ll want to carefully consider your unique requirements for personal property, loss of use, medical payments, and liability coverage. For your most valuable items, it’s worth looking into your Extra Coverage options.

Getting covered takes just minutes with Lemonade’s super-fast online sign-up process. You won’t just be buying America’s top-rated renters insurance at a refreshingly reasonable price, you’ll also be protecting your financial well-being.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage and discounts may not be available in all states.

Share